CBO: Obamacare 20% cheaper than they projected; *net* +24M people will have health insurance before Obama leaves office.

— Steven Dennis (@StevenTDennis) January 26, 2015

Cheaper, better, faster — not bad at all.

![]()

Come for the politics, stay for the snark.

CBO: Obamacare 20% cheaper than they projected; *net* +24M people will have health insurance before Obama leaves office.

— Steven Dennis (@StevenTDennis) January 26, 2015

Cheaper, better, faster — not bad at all.

We are interviewing some new Padawans. I’ve been asked to give them a high level overview of plumbing health insurance including how a newly built plan gets priced. I’ve been asked that same question here, so I’m prepping my class notes on Balloon Juice. The first few pieces will start with some massive simplifying assumptions that are completely unrealistic in the American context but will provide us with a simple pricing model to gain initial intuitive understanding. After we get a feel for how a plan is built in isolation, we’ll look at how several different knobs are twisted to tweak the results of a plan and its pricing. Finally, we’ll get a bit more complex and introduce competition to the model as well as dynamic interactions. I think there are at least three pieces here, but there will probably be more once I start writing.

The first and most basic assumption in the American context is that a plan will not be offered by an insurance company if it is a long term money loser. This assumption holds true for shareholder owned companies, it holds true for privately held companies, it holds true for co-ops, it holds true for non-profits, it holds true for national players, it holds true for regional players and it holds true for local niche insurers. No one will sell a product that loses money for long.

Let’s make a few simple and completely or mostly unrealistic working background assumptions. Assumption one is that there is a single price. Assumption two is that people can either take the insurance at a single price or decline it without penalty. Assumption three is that people have a better idea of their health condition than the insurer but there is some uncertainty. Assumption four is that health care costs are distributed unequally across the population with a power law distribution with a minimum of zero and a maximum somewhere north of $10,000,000. Assumption five is that people are generally risk averse. Next, the assumption is that the insurer is the only insurer in the region and everyone is currently uninsured. Finally, we’ll keep things simple and assume the plan is 100% fee for service. Yeah, these are some absurd assumptions.

I just want to reply to a couple of recent questions in comments:

A. Do the ACA substantive requirements for health insurance — no exclusion of pre-existing conditions, mandatory preventive care coverage, etc. — apply to all health insurance, or just to insurance bought on an exchange, like healthcare.gov?

No, but most commercially available insurance in general will meet the requirements. There are three major classes of insurance products which won’t meet all of the substantive requirements. The first are plans that were sold on or before PPACA was signed in March 2010. These plans are grandfathered. The grandfathered plans can continue to be offered as long as there is no substantial difference. Most grandfather plans will disappear over the next couple of years although I will be shocked if there is not some grandfathered plan with seven members still being sold in 2025. The second group of plans are group insurance plans that are self-insured. That means Big Mega Corp will contract with Mayhew Insurance to do the front end work, but Big Mega Corp pays all the bills and takes the risk of a $10,000,000 claim. Self-insured is fairly common at medium to large employers. Self-insured plans have far fewer requirements and regulations than fully insured plans. Fully insured means Big Mega Corp writes a big check to Mayhew Insurance and we bear the risk of paying out on a $10,000,000 claim. The final group of plans that won’t met all of the requirements are the closely held private firms that got profitable religion.

On the Individual market, there are very few grandfathered plans out there, and the other two categories don’t matter. Most of the plans are ACA compliant. Off-exchange has more variety than on-exchange, but the structure is very similar.

it turns out that this so-called “provider” is a Middleman Bill Processing Company. The actual provider sends the bill to this Middleman company, who then applies the discount, does the billing, and then sends it to the insurance company. Middleman Bill Processing Company shows up as the provider on the EOB.

What this also means is that the actual charges by the actual provider are obscured. I have no idea what the real Amount Billed is. The discount is not given. It’s all completely invisible. I got into an argument with the actual provider’s billing office because their billing rep thought I should be able to see this info. I could not.

So my question is: How is this legal or is it legal? How is it allowed for the “Provider” to be some anonymous Middleman Bill Processing Company?

This is legal and fairly common. Right now, Mayhew Insurance’s biggest single “provider” account is a claims processing company a time zone east of us. From a claims payment point of view, an insurance company needs a valid tax ID number, a valid national practitioner ID, a valid set of procedure codes and that is about it. Anything else is a bonus. From a claims point of view again, the charged amount or what the actual doc asks for is irrelevant. The amount paid will be the agreed amount between the insurer and the claims processing company for that set of codes and for that TIN. The allowed amount is what will count to deductible and co-pays and coinsurance, not the charged amount.

The medical loss ratio of the ACA stipulates that 80% of all insurance costs should be used for medical purposes, with 20% going for profits and overhead. That is billed as a cost saving device…. if the insurance plan can either pay for procedure A, costing 1000 dollars, and procedure B, costing 10,000 dollars, doesn’t it have an incentive to chose procedure B, allowing it to hike premiums next year and having the 20% it keeps become more valuable?

What am I missing?

Competition.

In states/regions where there are multiple insurers all trying to get and keep marketshare, if Company 1 pays $10,000 for procedure B while Company 2 pays $1,000, Company 2 will have much lower medical costs and thus lower premiums next year. It is extremely likely that Company 2 will have a Top-2 Silver product next year. That means people get full subsidy and very low out of pocket premium prices which means they get a lot of new membership from both the still uninsured pool as well as healthy membership from Company 1 as they are transferring.

This falls apart in states/regions with only a single insurer.

I’m happy that I’m probably going to be wrong about what I’ve written about Arkansas’ private option plan. I thought there would be a good chance that the private option and thus Medicaid expansion would be nixed in Arkansas because it has a strong majority coalition but an extremely fragile super-majority coalition in 2013 and 2014. The November elections tossed out a few marginal supporters and replaced them with Teabaggers who out-teabag Lipton, and the outgoing governor who championed the private option with an incoming governor who was non-committal about the entire thing.

I thought that meant the end of the private option after this year. I was wrong as the Arkansas Times explains that I was wrong in both the essence, and a critical detail as it looks like the Arkansas private option will get slightly less punitive and slightly better for people making under 100% of the federal poverty line.

He (the governor) is asking the legislature to fund the private option for two more years, and he’s asking for a legislative task force that would lead the way on an overhaul of the state’s health care system in 2017.

But there was also little piece of policy news buried in the bill filed yesterday by Hutchinson’s nephew (and previously outspoken opponent of the private option) Sen. Jim Hendren. If passed, Hendren’s bill would make a couple of tweaks to the existing private option. It would halt co-pays and the Health Independence Account program on private option beneficiaries below the poverty line, and it would nix future transitions of certain populations now on traditional Medicaid over to the private option.

Medicaid co-pays for people making under 100% of the federal poverty line tend to be nominal. Usually it will be $2 or $3 for office visits and prescriptions and up to $8 for emergency room visits that don’t result in admissions. Most states don’t enforce the co-pays and will reimburse providers for co-pays that weren’t paid. It is a massive administrative burden for little gain in either reduced costs per service or utilization reduction. Arkansas has tight eligibility requirements for Legacy Medicaid, so that population is probably sicker and more expensive than the current private option population. Keeping current Medicaid beneficiaries on Medicaid is an interesting choice as Arkansas pays a significant percentage of their care, while the Feds pick up the entire cost of care for current private options members, and will pay a higher percentage in the future. However, it also lowers the overall medical expense of the entire Exchange risk pool in the state, so it could lower net premiums.

Overall, I was wrong, and I am very glad to be wrong about Arkansas this week.

Unlike Aaron Carroll at the Incidental Economist, I was a policy and process analyst major in younger days. But we had the same concept of the binding constraint:

the rate limiting step. See, in any chemical reaction, there’s always one part that is the slowest. If you want to speed things up, you’re going to be able to make the most difference by focusing on that step….

I had to do laundry last night. We had an adult whites and towels load, an adult colors load, a referee load, and the kids load. The process is fairly simple; put clothes in washer, wait for washer to buzz, move clothes from washer to dryer, reload washer and wait for dryer to buzz. The binding constraint in that process flow is the dryer as it takes roughly two washer cycles for a dryer cycle.

In order to maximize the amount of sleep I got, I had to optimize the binding constraint. That meant I put all of the clothes in the washer on an extra five minute spin cycle to wring out as much moisture as possible. That meant that as soon as I heard the dryer buzz, I went downstairs and changed the loads to minimize its non-use, and it meant that I hung my jeans and towels out to finish drying instead of putting them back in the dryer for another twenty minutes. The dryer was idle for maybe five minutes from start to finish. The washing machine was idle for a significant portion of the time, but the process was nearly as efficient as possible because I optimized the usage of the binding constraint.

Aaron notes that we don’t focus on the binding constraints or the rate limiting step in health care:

Bill and Melinda Gates are doing it right. From 1990 to recently, the childhood mortality rate has been cut in half. Why? Cause they pay attention to the things that matter. What kills kids worldwide? Malaria – and they’re hard at work on a vaccine. No worries about phantom illnesses or the craze of the week. Instead, they’ve got a solid focus on the things that actually matter….No fancy new medicines. No genetic tests. And it’s easy to roll your eyes and say this is common sense stuff, and it is in much of the developed world. But I think the Gates want to do the most good they can for children worldwide, period. And they can do so by improving things for those who have it the worst. That’s the rate limiting step. Further, they can do the most good in the places that need it the most by focusing on the things that are actually killing kids. In this case, it’s nutrition, hygeine, and infection control….

Rocket science is cool if the goal is to go to Europa (even if we’re warned not to) but it is not a panacea. However the United States treats high end medical science as an end all and be-all. There is plenty of research to show that talking to patients about their goals, desires, and constraints leads to better health outcomes at lower cost and resource utilization that the best pill. There is plenty of research that shows wrapping social services around individuals at high risk lowers medical utilization and net spending than telling people to come to the emergency room if they feel ill. There is plenty of research that basic checklists minimize errors. Yet we don’t do that. It is easier to get a massive capital intensive installation than revamping business practices to emphasize the human and humane.

So we spend money on the sexy and the shiny instead of the simple and effective.

The lessons for the US are clear though. What’s the number one killer of kids in the US? Accidents – by far. But the number of foundations and NIH dollars going into that is miniscule. Know what consistently makes the top five? Suicide and homicide. How much time and money do we spend on researching ways to reduce that?

We don’t want to focus on those issues because of Freedumb ™.

If we focused on suicide and homicide that would mean that we actually have to talk about guns in a rational, adult manner where costs and benefits of having an absurdly heavily armed population is a reasonable thing to talk about. Instead of how guns are non-prescription Viagra or major tribal cultural markers. It would mean talking about how are communities are designed so that it is almost impossible for children to safely walk to the vast majority of their daily places of life. It would mean talking about mental health without stigma. It would mean that we as a society are also a community with shared responsibilities.

Those are evil and deviant thoughts so we chase shiny objects instead.

Andrew Sprung at Xpostfactoid has been doing the long and very valuable slog of figuring out average acturial value of what is being sold on the Exchange. Right now, once you factor in cost sharing assistance, the average acturial value of insurance being sold on the Exchange looks a lot like typical employer sponsored insurance:

only 20% of ACA private plan buyers in 2014 selected bronze plans, most of them probably in higher income brackets. By my estimate, over half of ACA buyers obtained plans with an actuarial value of 80% or higher, including about 90% of buyers with incomes under 200% of the Federal Poverty Level, who accessed Cost Sharing Reduction subsidies by buying silver plans. And while ACA coverage can have troubling limitations, from high deductibles to narrow networks, I just stumbled on information that indicates what an improvement the actuarial mandates constitute.

This 2012 study found that more than half of the health plans sold in the individual market in 2010 had actuarial values of less than 60%, and that 60% was the average AV of all plans sold on the individual market in that year. Many of the “rate-shocked” holders of canceled individual market plans who hit the news in fall 2013 probably had plans that were skimpier than ACA bronze

On Exchange are mostly people who qualify for subsidies. Acturial values in the mid-80s is an appropriate level of coverage for people as the actual shock of a big claim is mostly eaten up by the insurance. As a side note, the average AV of newly insurance people for PPACA will be even higher as Medicaid tends to have acturial values in the very high 90s, and that is roughly half of the newly covered people.

Off-Exchange is everything else. A person who is buying off Exchange is far less likely to have qualified for subsidies due to either making too much money, or immigration status. Here, moving acturial value from the 40s% or 50%s to 60% is a real increase in the value of the policy.

As I’ve said before, I’m not a big fan of high deductible health plans (HDHPs) or catastrophic coverage for most people. Typically, I’m only in favor of HDHPs for people who are very healthy and have access to financial resources to cover a kick in the balls claim on their deductible. The off-exchange buyers that had previous underwritten coverage and who don’t qualify for subsidies because they make too much money is one of the few easily identifiable clusters of people where a HDHP/catastrophic coverage scheme makes a lot of sense.

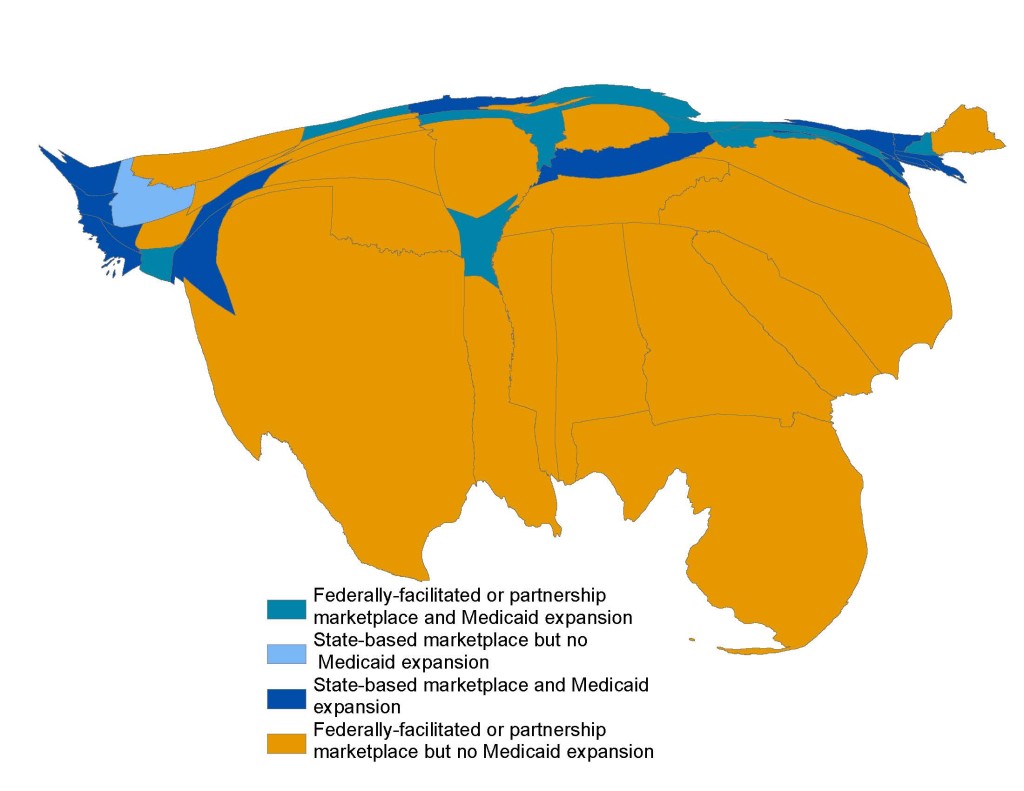

Harold Pollack at Same Facts has a great map that shows where making Medicaid expansion optional is hurting people.

We know the upper Mountain West is looking for ways to tweak and twist their Medicaid programs to align with both conservative policy goals and liberal coverage expansion. We know Maine has an asshole for a governor but a non-veto proof majority in the Legislature that is pushing for Expansion. We know Virginia has a split political elite that is slightly tilted against expansion. But the Deep South is where there is a wide spread elite political consensus that it is best for their political leaders to stand in the hospital doors to prevent poor people from getting healthcare. Arkansas is looking to regress from its expensive and convoluted but successful private option implementation to either nothing or far less for its poor citizens.

This was predictable, reactionary states that run on extraction economies and have a political history of nullification would nullify laws that threaten elite privilege however they could. And the Roberts Court narrowly but consistently is providing a set of tools for nullification to work.