Picking insurance is tough. It involves an ungodly number of trade-offs and incredible amounts of decision making under uncertainty for most people. Some people have an “easier” task because they know that they are facing a $500,000 claim year no matter what so their problem is a well defined and well constrained optimization problem. Most people are luckier in that they aren’t facing a guaranteed OMG claim year but this makes the optimization problem far fuzzier.

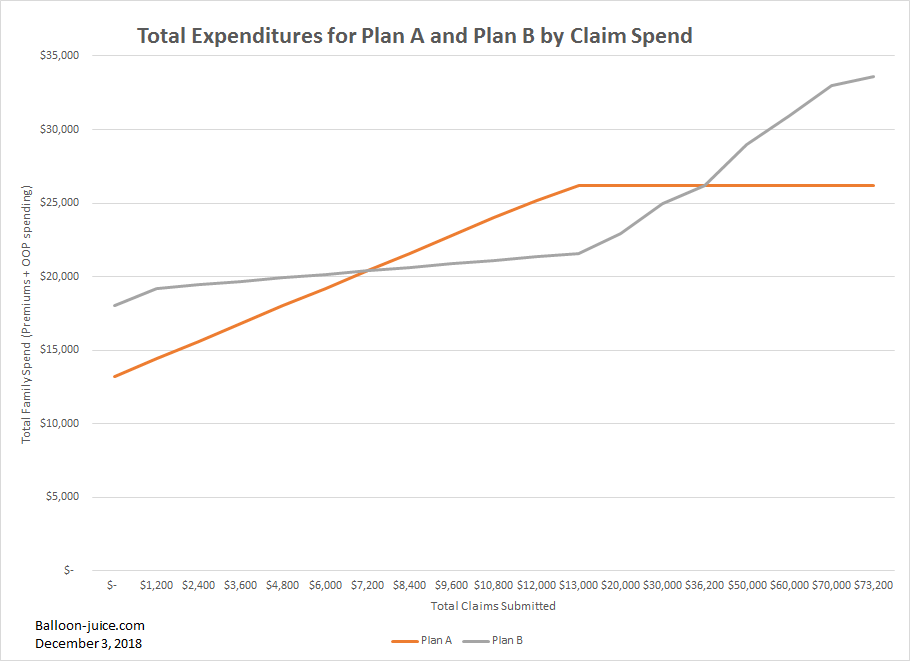

Which plan is better for your family? Let’s assume that the two hypothetical plans below are from the same insurer with the same network, plan type and otherwise identical details except for the pricing and the cost sharing. The cost sharing is very simple; everything goes to deductible and then if there is a co-insurance, it applies to every claim above the deductible amount and below the out of pocket maximum amount. This is a simplification but I think it will provide useful insight.

| Plan A | Plan B | |

| Monthly Premium | $ 1,100 | $ 1,500 |

| Annual Premium | $ 13,200 | $ 18,000 |

| Deductible | $ 13,000 | $ 2,400 |

| Coinsurance | 0 | 20% |

| Max OOP | $ 13,000 | $ 15,600 |

Plan A has a lower premium but a higher deductible. Plan B has a higher premium, a lower deductible but co-insurance that builds to a higher maximum out of pocket expense.

Which plan is better?

Well it depends….

Plan cost sharing, premiums and superiority zonesPost + Comments (17)