In 2019, 1,058 counties had only a single insurer on Healthcare.gov. 1,056 of those counties had the insurer offer at least one Silver and one non-Silver plan. I am curious about what we can figure out about the monopoly insurer strategies. I’ve contended for years that a monopolistic insurer can effectively choose their enrollee pool by how they manipulate the spreads from the benchmark plan to the other plans.

Insurers can choose their risk pool by offering very low cost plans. The people who are on the cusp of buying insurance are price sensitive. The healthiest slice of the cohort will be the people who are flipping a coin between buying insurance and not buying insurance. The sickest slice of the cohort will be the people who look at a $1,500 monthly premium and are doing a happy dance as they know they are still getting a great deal. The risk pool will be, on average, healthier if the cheapest plan available costs $15 for the incremental buyer rather than $100.

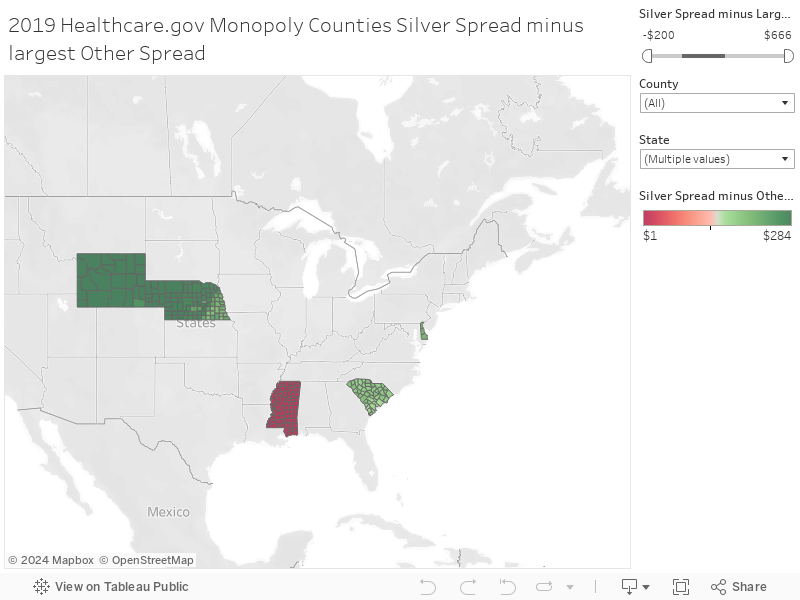

Monopoly insurers get to choose their spreads**.

So this is very curious when I look at the difference between the Silver Spread which is the difference of the Benchmark Premium to the cheapest Silver premium and the Other Metal Spread which is the difference of the Benchmark Premium to the Cheapest Gold/Bronze premium for 2019.

There is wild variance. A few counties in Wisconsin and Ohio have no Bronze plans. Their cheapest not-Silver plan is significantly above the cheapest Silver plan.

Wyoming, on the other hand, is running a massive spread so that their cheapest Bronze plan has a significantly lower subsidized premium than the cheapest Silver plan.

One of the big things to note is that insurers that are operating as effectively a state wide individual market monopoly do not have to consider risk adjustment in their decisions. Insurers that are in a fragmented state wide market with only a county or regional monopoly may have risk adjustment concerns.

This risk adjustment concern leads me to scratch my head when I look at the different strategies that are evident in Mississippi and Wyoming. Both are single insurer states. Wyoming’s Exchange strategy creates very low premium for subsidized buyers who are flipping a coin. Lots of people earning between 100% to 400% federal poverty level are seeing Bronze and some Gold plans that will cost them and their families less than two medium three topping pizzas at a national delivery chain every month.

Mississippi is also a single insurer monopoly state. There is a different pricing strategy. The Gold plans are priced over the benchmark silvers as they broad load. The low cost Bronze plans are creating very few truly low premium plans.

I am confused as pure monopoly ACA insurers that have no risk adjustment concerns should be able to create their own risk pools for whatever purpose they so choose. They can choose a sick pool. They can choose a healthy pool. They can choose a small pool. They can choose a big pool. Wyoming’s pricing and plan offering strategy is a choice to pick a big and comparatively healthy pool. Mississippi’s sole insurer, Centene, is picking a comparatively small and comparatively unhealthy pool.

That just seems odd to me.

** I am using a single 40 year old non-smoker non-subsidized for all examples. For purposes of the blog, I am not looking into EHB percentage of premium which will slightly alter final numbers.