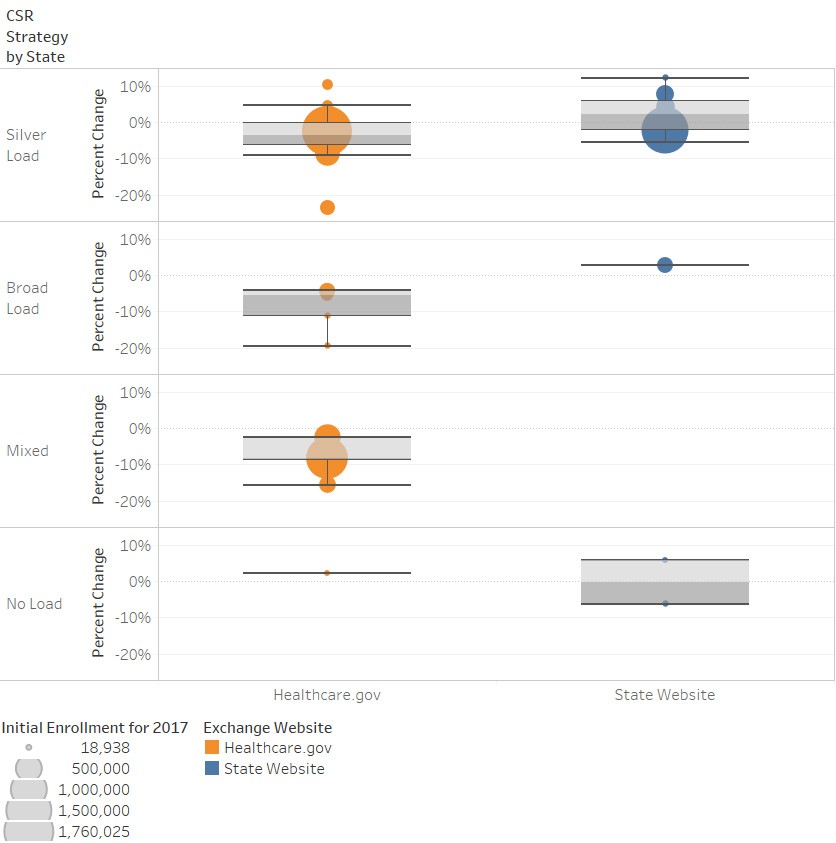

One of the major challenges of the Exchanges going forward will be the morbidity of the risk pools. I am modestly concerned about the size and health of the well subsidized component of the risk pools. I am very concerned about the size and average health of the low or no subsidy components of the risk pool.

Katie Keith at Health Affairs summarized two recent actuarial studies on the impact of expanding underwriting and the removal of the federal individual mandate:

Two new analyses—issued by the actuarial firms Wakely and Oliver Wyman—examine the impact that the proposed rule, if finalized, would have on the Affordable Care Act’s (ACA’s) individual market. Both find the impact to be much higher than federal estimates, which is consistent with a previous analysis from the Urban Institute….

Wakely’s report modeled three different scenarios…Combined with the repeal of the individual mandate penalty, premiums would increase by up to 12.8 percent and enrollment in the ACA market would decrease by up to 26.3 percent.

Wakely’s findings are consistent with an analysis from Oliver Wyman on behalf of the D.C. Health Benefit Exchange Authority. Oliver Wyman found that the proposed rule alone would increase claim costs in D.C.’s individual market by up to 3.1 percent; enrollment in the city’s individual market would decline by 900 people. Combined with repeal of the individual mandate penalty, claim costs would increase further, up to 21.4 percent, and enrollment would decline by about 6,100.

Both analysis show that healthy, low cost individuals will leave the ACA market. Some will be uninsured and others will get low premium, underwritten plans. For well subsidized buyers, this won’t matter too much as the federal government eats all of the premium price hikes. For non-subsidized buyers they get whacked with massive premium increases.

States are taking action to temper some of these increases. Republican controlled Wisconsin submitted a reinsurance 1332 waiver that will hold lead to a 10% decrease in premiums compared to no other action. New Jersey’s legislature just passed a state level individual mandate and authorized a reinsurance 1332 waiver application.

These are reasonable and appropriate steps to keep some of the non-subsidized premiums from increasing even faster. They also require significant state funding.

I am curious if states that want to do something but either can not or will not find state funding can go an alternative route to provide some minimal assistance to indviduals who do not qualify for subsidies but who will not pass underwriting. Can states apply for a 1332 waiver that allows for the creation of Off-Exchange only Copper(50%) and/or Tin (40% AV) plans that are tied into the common risk adjustment pool.

There are two angles here that could provide at least incremental relief. First, slightly lower cost plans with high out of pocket expenses will bring in slightly more people who are reasonably healthy which will bring down the total average morbidity slightly. This is a bankshot.

Secondly, the ACA’s low actuarial value plans (Bronze) are a really good deal for two classes of unsubsidized people: those who anticipate very little healthcare needs for a year and those who anticipate an incredible amount of healthcare needs. For the first cohort, they are buying solely on premium. A Copper plan will be more attractive to them than a Bronze plan as the incremental out of pocket maximum is barely relevant while the decrease in premium is very real. People who know that they need lots of expensive care have a more complex calculation. They are optimizing on the minimal total cost (premiums plus out of pocket maximum) of plans with a minimally sufficient network.

Last October we looked at the Healthcare.gov counties and some variant of Bronze is the least expensive choice for most middle aged individuals who are highly likely to max out their benefits.

For someone who knows that they are facing a $50,000 claim year, the lower premiums of a Copper plan may lower total costs even as out of pocket maximums increase. IF they do, the person is better off going Copper instead of Bronze. If not, they are no worse off.

So can states file a 1332 that allows for the offering of a Copper plan off-Exchange only?