Let’s talk about something not likely to tear apart the comment section — ACA risk adjustment!

Earlier this week, the Centers for Medicare and Medicaid Services released their 2023 risk adjustment summary for ACA regulated plans. The ACA requires insurers whose population codes as healthier/lower cost than the state average to send money to insurers whose population codes as less healthy/more expensive than the state average. The program intention is to make insurers, on net, to be risk agnostic. With perfect risk adjustment, an insurer should not care if they are covering a 63 year old with a medical history that looks like a CVS receipt or a 23 year old who has not seen a doctor in five years and feels great. We don’t have perfect risk adjustment.

One program feature of the ACA risk adjustment system is that it is zero sum within a state. It is all between insurer transfers minus a tiny (<$1 per member per month) administrative fee that is paid to CMS to run the program. There is no new federal money being added to the system. There is a strong implied assumption that insurers that owe money will be around to pay insurers that are counting on that money to pay claims.

That does not always happen.

Last year, FRIDAY HEALTH PLAN shut down mid-year as it had massively overexpanded and was losing money hand over fist. FRIDAY was able to do this even as they covered a very healthy, low using population.

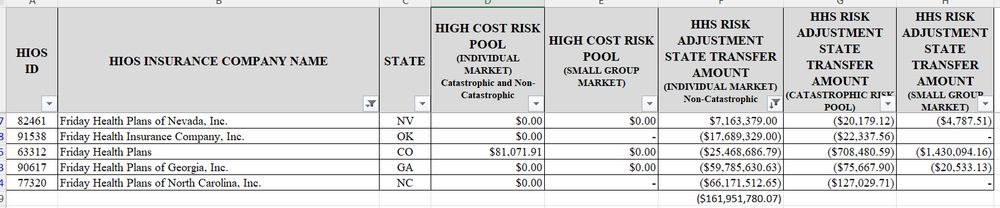

And now the insurers that were covering the sick people in the states where FRIDAY blew up are holding the bag:

In four out of the five states where FRIDAY was operating, they covered a healthier than average population. On net, they owe $161+ million dollars that are very unlikely to be recovered by other insurers.

The insurers that took on medical risk also took on low cost/low acuity competitors blowing up risk. The insurers in North Carolina that are in a net receivable position are all very well capitalized insurers so it won’t lead to system failures, but the incentives are to go low and race to the bottom. Not compensating insurers for taking on risk leads them to not want to take on risk.