Susan Collins thinks her supporters are suckers.

We don’t.

Let’s make 2020 as unpleasant as possible for her.

And also the core organizing principal should be that “these go to 11” in a world where “51 and Fuck you” is the most recent precedent:

![]()

Come for the politics, stay for the snark.

I am a student in the doctoral program at the Duke University Department of Population Health Sciences. I am working towards my my doctorate in Health Services Research with a policy focus. I am fundamentally fascinated by insurance markets, consumer choice and the navigation of complex choice environments. I'm currently RA-ing at the Duke Margolis Center for Health Policy.

I used to be Richard Mayhew, a mid-level bureaucrat at UPMC Health Plan. I started writing here and have not found a reason to stop.

Conflicts of interest: Previously employed at UPMC Health Plan until 12/31/16. I also worked full time as a research associate at the Duke University Margolis Center for Health Policy. I have received direct funding from the National Institute for Healthcare Management, and I have been on projects funded by the Rockefeller Foundation, Kate B. Reynolds Charitable Trust, Gordan and Betty Moore Foundation, Duke University Health System, CMMI, and various value based payment consortiums. I serve as a consultant on a grant from the Commonwealth Fund and have acted as a consultant to several ACA insurers.

Research Production is here: https://scholar.google.com/citations?user=zof9b4IAAAAJ&hl=en

David Anderson has been a Balloon Juice writer since 2013.

Susan Collins thinks her supporters are suckers.

We don’t.

Let’s make 2020 as unpleasant as possible for her.

And also the core organizing principal should be that “these go to 11” in a world where “51 and Fuck you” is the most recent precedent:

Earlier this week, I noted that the ACA risk adjustment program is highly likely to overpay for Hep-C anti-viral prescriptions this year and next year due to list price reduction shocks. The price that insurers pay will be significantly below the prices used to determine risk-adjustment co-efficients.

We had briefly talked about a great NBER paper by Geruso, Layton and Prinz in June 2017 about how risk adjustment and reinsurance mostly worked on the ACA to remove cherry picking incentives. My thought when I read the paper was that this was a profit-making opportunity for positive risk screening for certain small groups of drugs:

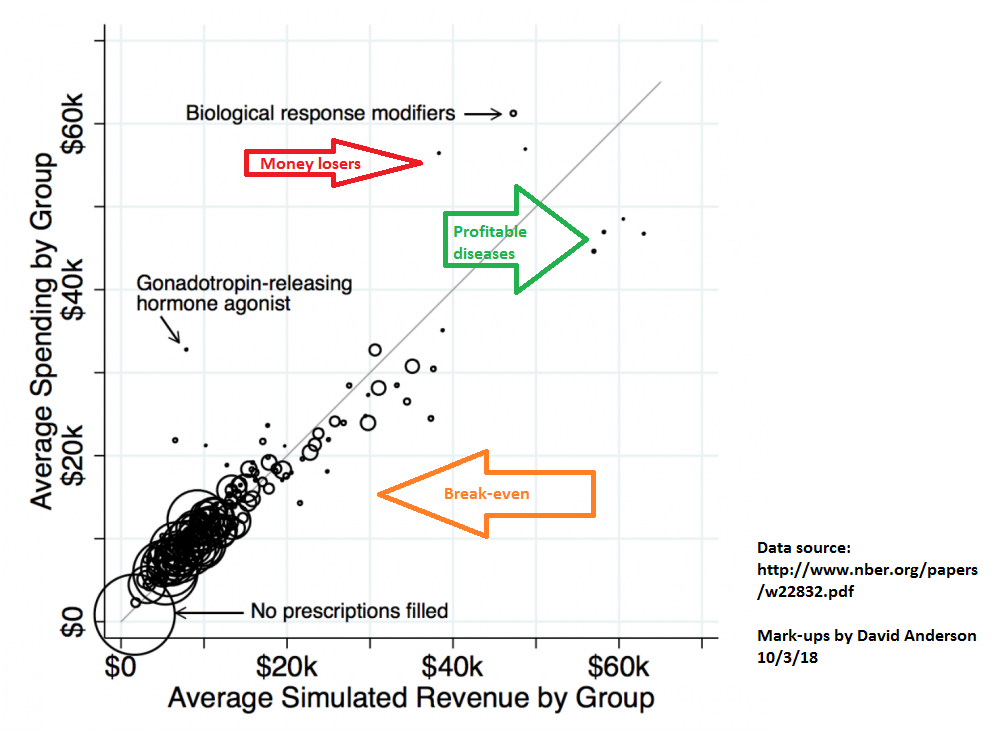

I had my cynical bastard insurance company plumber hat on as I looked at that graph. There are several drugs in that lead to a total cost of treatment between $45,000 and $50,000 but bring in between $55,000 and $65,000 in revenue. They are the massive beneficiaries of risk adjustment.

My big operational question is whether or not insurers were actively designing formularies to attract these patients?

I want to repost a slightly modified version of the graph that I referenced in order to talk a bit more about this idea of attracting profitable risk:

Every circle near the gray line is risk adjustment and reinsurance working close enough to right; total net incremental revenue is close enough to total net incremental costs. The dots that are noticably above the gray lines are risk adjustment and reinsurance problems where total net incremental revenue is significantly below total net incremental costs. The dots below the gray line and near the green arrow are profitable drug classes as the net revenue (premiums plus reinsurance plus risk adjustment) is significantly more than the incremental costs of care.

Every circle near the gray line is risk adjustment and reinsurance working close enough to right; total net incremental revenue is close enough to total net incremental costs. The dots that are noticably above the gray lines are risk adjustment and reinsurance problems where total net incremental revenue is significantly below total net incremental costs. The dots below the gray line and near the green arrow are profitable drug classes as the net revenue (premiums plus reinsurance plus risk adjustment) is significantly more than the incremental costs of care.

I think that the ACA risk adjustment formula with the currently lagged data is moving Hep-C cures into this group for a couple of years. Insurers should have strong incentives to make it very easy for anyone that they cover in the ACA individual market to get easy access to the Hep-C cures as it will be very profitable for the insurers to do so. I think one of the first tests that we should expect to see will be if there is a drop in tiering and pre-authorization requirements for at least one of the drugs in the Hep-C anti-virals therapeautic class. If that is the case, then we can probably infer that an insurer is more willing to pay-out on Hep-C risk.

New Mexico is preparing for an ambitious future for health policy. Louise Norris notes that New Mexico is looking to move off of Healthcare.gov and open up their own state based exchange.

In order to reduce user fees, the exchange board considered the issue during a September 2018 board meeting, and voted unanimously to transition to a fully state-run exchange in time for the 2021 plan year.

The exchange will put out a request for proposals in early 2019, as they work to find a vendor to create their state-run enrollment platform. The system will be live by the fall of 2020, in time for the open enrollment period for 2021 coverage (November-December 2020).

There are two good reasons to go down this path. The first is the obvious one: it’s cheaper than using Healthcare.gov. Healthcare.gov charges 3.5% of premium as an Exchange fee for states that don’t do anything on their own, and a 3.0% of premium Exchange fee for states that manage significant elements of the enrollment process. New Mexico is one of the “partnership” states that uses the Healthcare.gov front-end but manages a lot of their own back-end. 3.0% of premium is not a good deal. The same fee level would either be used to fund significantly more outreach, advertising and navigators or the same level of outreach and support that Healthcare.gov provides could be funded at a much lower fee which would slightly reduce baseline premiums.

Secondly, New Mexico is getting ambitious. They are the leading innovators in doing the actual hard work of figuring out how a Medicaid buy-in proposal. This would be effectively a state based public option. This would be a major rejiggering of the New Mexico individual market.

The Center for Medicare and Medicaid Services (CMS) has repeatedly stated under both the Obama and the Trump administrations that they can’t do much with the back-end of Healthcare.gov to support unusual or aggressive waiver requests. If New Mexico moves towards a Medicaid buy-in model, their open enrollment, subsidy structure and eligibility structures would be unique. The only way that can work within an Exchange framework is if New Mexico can customize the exchange that their citizens and residents see.

So, this is both an effort to reduce premiums through either attracting a healthier risk pool or lower costs of attracting the current risk pool AND a necessary step in building the infrastructure to support a Medicaid buy-in program.

I’ve been busy this week at Health Affairs. The big piece at the HA Blog is an overview of the new Basic Health Program rule that the Center for Medicare and Medicaid Services (CMS) issued in August. Dr. Lynn Blewett and I went over how the BHP funding stream is predicated on the counterfactual of a fully offered Qualified Health Plan (QHP) market and not the actual premiums in that market. That would have been an esoteric point from 2014-2017 but it is critical in 2018 and beyond as Cost Sharing Reduction (CSR) subsidies are not being paid:

In December 2017, CMS notified Minnesota and New York that it would no longer fund the cost-sharing reduction component of the BHP payment formula, citing the lack of congressional appropriations for cost-sharing reductions. CMS stopped payments for the first quarter of 2018. The states initially asked CMS to revise its calculation to reflect a higher “premium tax credit” portion of the BHP payment due to the effects of silver-loading….

The new payment methodology provides an 18.8 percent adjustment to the BHP payment for both Minnesota and New York. CMS cites Section 1331 to add a new plan adjustment factor based on the experience of other states with a special focus on enrollees with incomes below 200 percent of poverty. Section 1331 requires CMS to “take into consideration the experience of other states with respect to participation in an exchange and such [premium tax credits] and [cost-sharing reductions] provided to residents of the other states.” CMS uses this provision as its rationale for examining the effects of silver-loading in other states and imputing those to BHP payments in Minnesota and New York…

I also have a letter to the editor in the most recent issue of Health Affairs that comments on Dr. Jessica Van Parys recent article on monopoly pricing. I am concerned about using the time series of 2014-2018 as an analytical approach as 2018 was just too goddamn weird from a pricing and competitive region perspective. Insurers did not know what the rules were so they either ran like hell (and are re-entering in 2019 now that the new rule set is known) or raised rates very aggressively.

Basic Health Program and Market Concentration notesPost + Comments (1)

A few weeks ago, Gilead Pharmaceuticals announced that they were creating an authorized generic version of Harvoni with a list price of $24,000.

In the case of Harvoni and Epclusa, which carry list prices of $94,500 and $75,000, respectively, the $24,000 price tag for a course of treatment with the generics is roughly equal to the net price paid by many insurers…

There are a lot of interesting nuggets to pull out of this. The most obvious is that list price and actual price are at best tenuously connected. The second point is that the average cost of treatment for a Hep-C cure is someplace under $30,000 once all of the behind the scene deal making is accounted for. Thirdly, this is a case where me-too/look-alike drugs actually have created a very viable, competitive market.

What I am most interested in is the risk adjustment games that can be played with a new, much lower list price (even if the effective net price is close to the same as before).

Risk adjustment for the ACA, Medicare and Medicaid use claims from the past to predict incremental cost increments for different disease and therapeutic drug classes. Pharmacy claims are based on the list price and not the net price. Risk adjustment co-efficiencts lag reality. This works well when the treatment modality is reasonably constant and pricing does not have a huge shock.

Oops… that is precisely what will happen with Hep-C. Right now, Hep-C antivirals risk adjust on the ACA individual markets at about a co-efficient of 39. Someone picking up a Sovaldi, Harvoni or any other Hep-C antiviral cure gets a risk score that predicts their annual costs will be about 39 times average statewide premium.

That co-efficienct is based on the last three years of available data and it is a blend of commercial and Exchange information. The list price of the Hep-C drugs for this period was over $80,000 per dose.

Insurers have been fairly aggressive in shifting their formularies to lower net cost to them Hep-C anti-virals. I would expect that insurers will aggressively push for the authorized generics for a risk adjustment edge. If the list price collapses to $24,000 there is a huge arbitrage wedge that insurers can exploit for at least 2019 if not also in 2020. They can get credit for $84,000 or $95,000 treatments while only paying out $24,000.

This advantages insurers that can both aggressively identify and treat folks with Hep-C. It also advantages insurers that have very good pharmacy benefit management that can get a really good net price on Hep-C anti-virals as it creates a bigger wedge to exploit.

On net, this type of wedge will incrementally encourage more Hep-C treatments to be approved and taken for folks who are in the ACA individual market for 2019 and perhaps in 2020 until the risk adjustment co-efficiencts catch up to the pricing/technology/legal shock of low list price authorized generics.

Generic Harvoni, Hep-C and risk adjustmentPost + Comments (16)

Last week HHS Secretary Azar bragged that the benchmark premium for the 2nd least expensive Silver plan on Healthcare.gov went down by 2% for 2019 compared to 2018.

That is good news for the US Treasury. A lower benchmark premium means smaller premium tax credits.

It might be good news for non-subsidized buyers as some plans are now cheaper.

It is slightly bad news for states with either a 1332 reinsurance waiver or a Basic Health Program (BHP).

It is either indifference or slightly bad news for subsidized buyers.

States that rely on pass through funding for either 1332 or BHP have an incentive to want high benchmark premiums in order to generate large pass through amounts that can be used for reinsurance or for the expansion of pseudo-Medicaid to 200% FPL which is the BHP program.

Individuals who get subsidies don’t care at all about benchmark levels. They care instead about the price spread between the benchmark plan and all of their other choices. Subsidized buyers are indifferent to the following two pricing scenarios:

| Subsidized Buyer Indifference Spreads | Low Premium | High Premium |

| Bronze | $ 400 | $ 600 |

| Silver 1 | $ 500 | $ 700 |

| Silver Benchmark | $ 525 | $ 725 |

| Gold | $ 600 | $ 800 |

This price indifference is the core resiliency feature of the ACA that allowed it to muddle through in 2018.

I think that as more insurers enter and re-enter markets and the Silver gaps compress again due to more competition, we’ll see fewer subsidized buyers than we otherwise would have seen and a slight increase in the number of non-subsidized buyers.

Ground breaking new study that shows an unexpected outcome from regular vaccinations. The visual abstract is below:

I love our pediatrician’s shirt today https://t.co/uchPBJhIdy pic.twitter.com/LIyFapwd98

— CoolPics (@CoolPics) September 25, 2018

Open thread as I’m off for a couple of days taking my kids to a magical land where the youth had to stand up against a reactionary revolt and a blinkered establishment willing to get played instead of disturbing the arrangements of power that had worked well enough.