There are strong rumors that President Trump will issue an executive order that will allow individuals to buy association health plans. These plans are not regulated by the ACA, instead they are regulated by ERISA. If the executive order or the subsequent rule making that comes from the order are upheld in court, these plans would be allowed to medically underwrite and risk rate their premiums.

So what does that mean for people who are looking to buy insurance on the individual market?

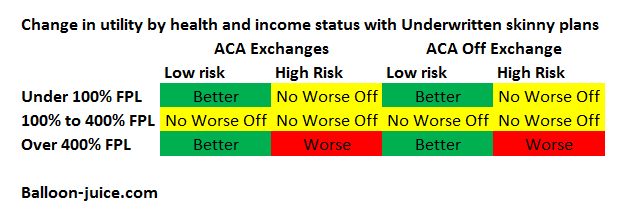

We need to split the universe of buyers into two risk groupings:high risk and low risk. Low risk individuals will get good underwritten rates and high risk individuals will get bad underwritten rates. Risk can be a function of medical history, hobbies, zip code, age or any other factor that an insurer has ever used to divide their risk pool. I think that we also need to divide the universe into three income groups. People who make too little for Exchange subsidies, people who make just enough for Exchange subsidies and people who make too much for Exchange subsidies.

I want to look through the distributional implications prospectively first:

Distributional benefits of underwriting in the ACA worldPost + Comments (20)