The Kaiser Family Foundation has put out a report

NEW: Workers’ out-of-pocket costs increasing faster than costs paid by insurers for job-based #healthinsurance https://t.co/2lIA4UviQi

— Kaiser Family Found (@KaiserFamFound) April 14, 2016

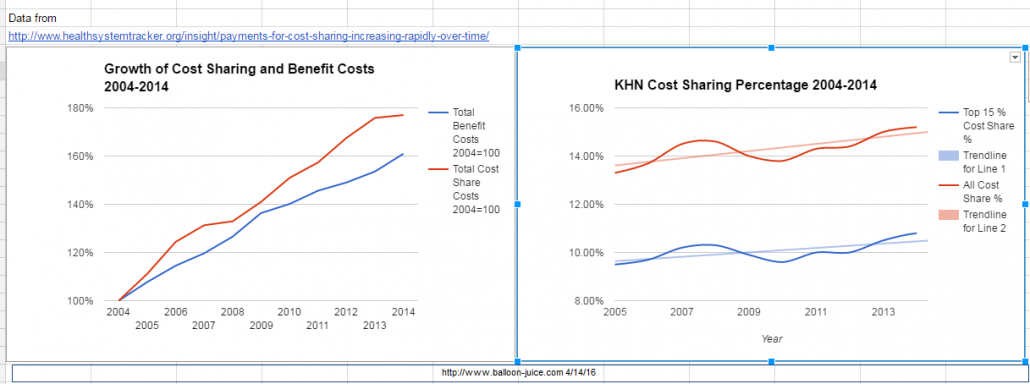

This looks like a crisis as deductibles have more than doubled. However percentages can be funny things, and thankfully the source data was in the report and I could play with it in a spreadsheet:. My big question was why did KHN break things out by type of cost sharing. So I combined cost sharing types and then got total benefit growth and total cost sharing growth using the same data but spliced a bit differently.

This is a different story.

There are two big things. First the cost of the total benefit which is cost-sharing plus what the insurer pays out has increased faster than the economy. Secondly, the actuarial value of used coverage has stayed fairly constant with a slight trend towards a higher proportion of all costs paid for by cost sharing. The red line on the first graph as it increases at a higher slope than the blue line informs the conclusion on the right hand side graph.

From here the problem is not that deductibles are too high because if we hold cost sharing percentages constant but still seeing significant cost growth deductibles versus co-insurance versus co-payments is mostly an allocation and incentive issue. The problem is that cost growth is too high and everything else flows from there. Larry Levitt made the point on the KFF chart that the interesting thing was the switch from quantity variant co-payments to total price variant co-insurance is a big deal as it does change incentives.

There are distributional concerns about cost-sharing choices. I’m probably in the minority in that I think deductibles are preferable than co-insurance and co-pays for a given percentage of cost sharing that must be borne by the entire user pool:

Deductible plans favor the sickest people as the low utilizers pay for almost all of their care via deductible cash. That means the proportion of the pool’s individual responsibility amount is borne by healthy people.

Co-pay only plans favor people who use highly concentrated cost services. A co-pay does not differentiate between a specialist visit with a contract expense of $200 and a specialist visit with a contract expense of $600. It is the same fee. So people who use very costly services but only rarely are best off. People who use a lot of fairly low costs services on a regular basis pay more proportionally.

Co-insurance only plans favor low cost utilizers. They are not paying full price via their deductible, and unlike co-pays, the individual cost per unit matters. Finally, No Use Nora is extremely valuable to the insurance company and the rest of the pool as she is fully cross subsidizing everyone else for this time period no matter how her benefits are built….

The other key insight of this exercise is that the non-covered actuarial value of a plan will get paid somehow by someone. The question is who pays and how much? If the objection to a deductible level is the size of the level, the problem is not the deductible, the problem is the low actuarial value of the plan.

The problem is not the cost sharing choices per se. The problem is medical care costs too damn much per unit of care. Almost everything else derives from that problem.