The Affordable Care Act’s subsidy system only applies to benefits that are categorized as part of the Essential Health Benefits (EHB). EHBs are determined by each state and they vary. Typically the EHB package is benchmarked against the benefit set of a commonly sold commercial plan in the state. Insurers have the option of adding benefits to any policy that they sell. These are called non-EHB benefits and the buyer, even if subsidized, has to pay the full incremental price. Some states require non-EHB benefits. The most common state-mandated non-EHB benefit is elective abortion coverage. However there are other non-EHB benefits and these can prevent individuals from being exposed to zero premium plans.

Zero premium plans have notable length of coverage effects due to lower administrative burden. Zero premium plans for individuals earning under 150% FPL have always been available but mostly have been Bronze plans. The under 150% FPL cohort has been buying Silver CSR plans overwhelmingly so these plans are not particularly relevant. However, under the new House Ways and Means committee reconciliation draft, a household earning under 150% FPL would be expected to pay nothing for the EHB component of the benchmark CSR eligible silver plan. Zero premium plans would proliferate.

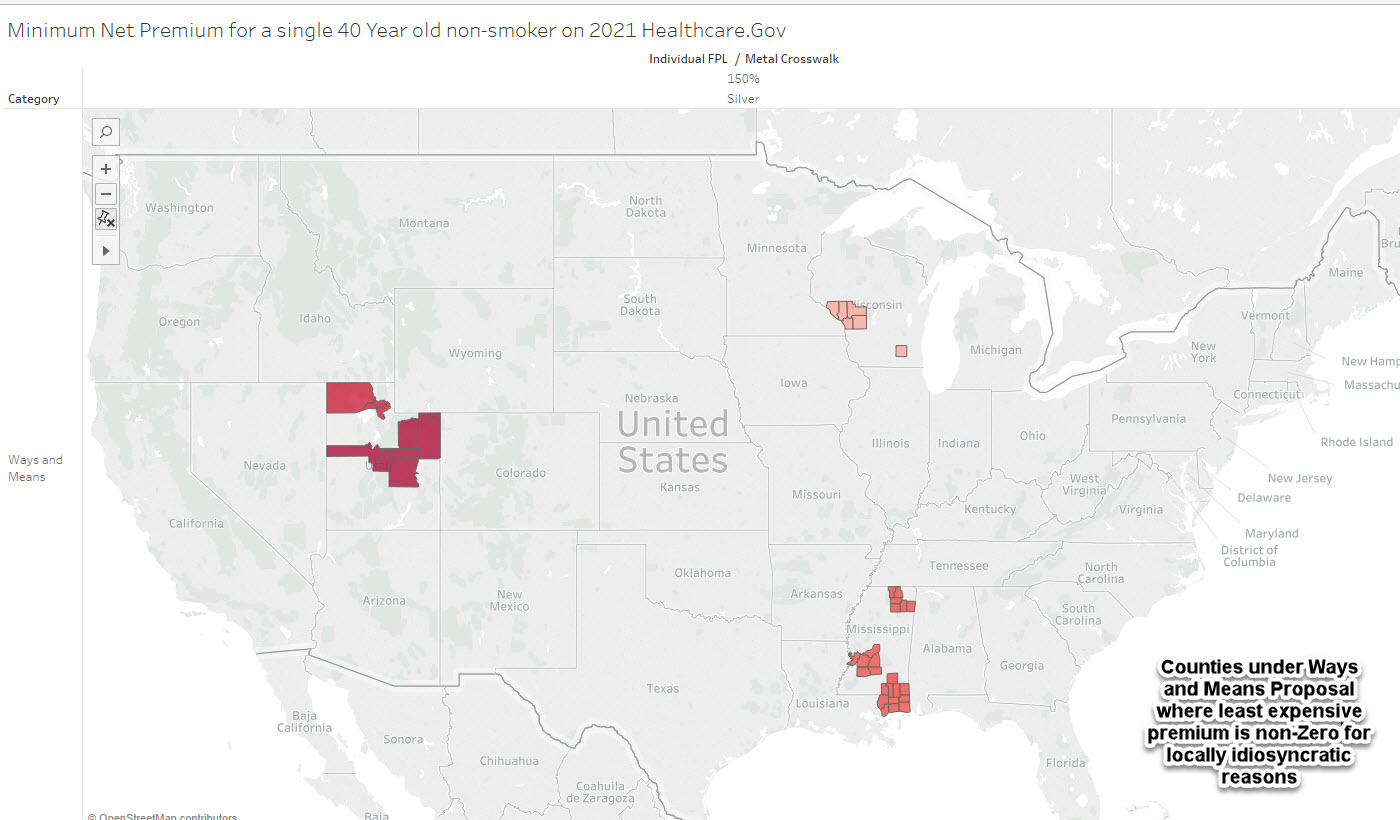

But there are pockets across the country where zero-premium plans are not occurring. Some states require elective abortion coverage. The cheapest plan will be a dollar per month to cover these benefits. However, other states, like Utah does not require elective abortion coverage. Insurers are allowed to design their plans to be all-EHB or add in non-EHB plans.

We see this in Box Elder County Utah and La Crosse County Wisconsin where insurers offer the benchmark and least expensive silver plans (EHB component only) but have very small added non-EHB benefit categories. In Box Elder County, these benefits add $1.36 per month in premium for a single 40 year old non-smoker. In La Crosse County, these added benefits add $0.16 in premium. Other insurers in each of these counties offer 100% EHB only plans. These are tiny benefits. However they are benefits that impose comparatively massive transaction costs.

We know that new buyers are mostly price sensitive. New buyers will buy the cheapest thing available. In most of the country, the cheapest thing available to families earning 150% of less with the Ways and Means proposal will be a choice of two zero premium silver plans. However this will not be universally true. It is not true in states where insurers must offer coverage of elective abortions due to the politics of Hyde/Stupak. There states are trading off administrative burden and access to a needed but politically fraught medical service. It is not true in chunks of Wisconsin, Mississippi, and Utah on Healthcare.gov where insurers that offer the least expensive or benchmark EHB component silver add on non-EHB services. This is problematic as there is little policy trade-off for a $0.16 per month benefit and several orders of magnitude greater administrative burden.

If I was the insurance dictator for a day in these states, I would require insurers to offer EHB only plans for their cheapest offering in each market. If they see a significant business case to add a minor benefit that is not subsidy eligible, then they could add it as the 2nd or 44th price ranked option (actually I would have something to say about offering 44 plans too).

Choosing insurance is tough. Imposing disproprortionate burdens for no gains makes it even tougher.

Added benefits and non-zero premium plans on the ACAPost + Comments (13)