Pennsylvania released their 2018 ACA rates on Monday afternoon. Their data is here (XLSM file) and the press release is here. They are explicitly Silver Switching the entire state to accommodate the CSR cut-off.

Because cost-sharing reductions are only available on silver plans, rate increases necessitated by the non-payment of these cost-reductions will be limited to silver plans. On-exchange bronze, gold, and platinum plans and off-exchange silver plans will not be impacted by these disproportionate increases.

Premium subsidies are calculated based on the cost of silver plans in each rating area, and subsidies increase in connection with rate increases. Because rates are rising on silver plans due to cost-sharing reduction non-payment, premium subsidies may be generous enough to allow an individual who qualifies to purchase a gold-level plan that has more favorable cost-sharing at a lower price than previous years.

Acting Commissioner Altman strongly encouraged individuals who do not qualify for premium subsidies to consider off-exchange options. The department worked with each of Pennsylvania’s five marketplace health insurers to ensure they would offer an off-exchange only option that is not impacted by the disproportionate rate increases for on-exchange silver plans. Off-exchange plans must be purchased directly through one of Pennsylvania’s five marketplace insurers or through an agent or broker licensed by the department to sell on behalf of these companies.

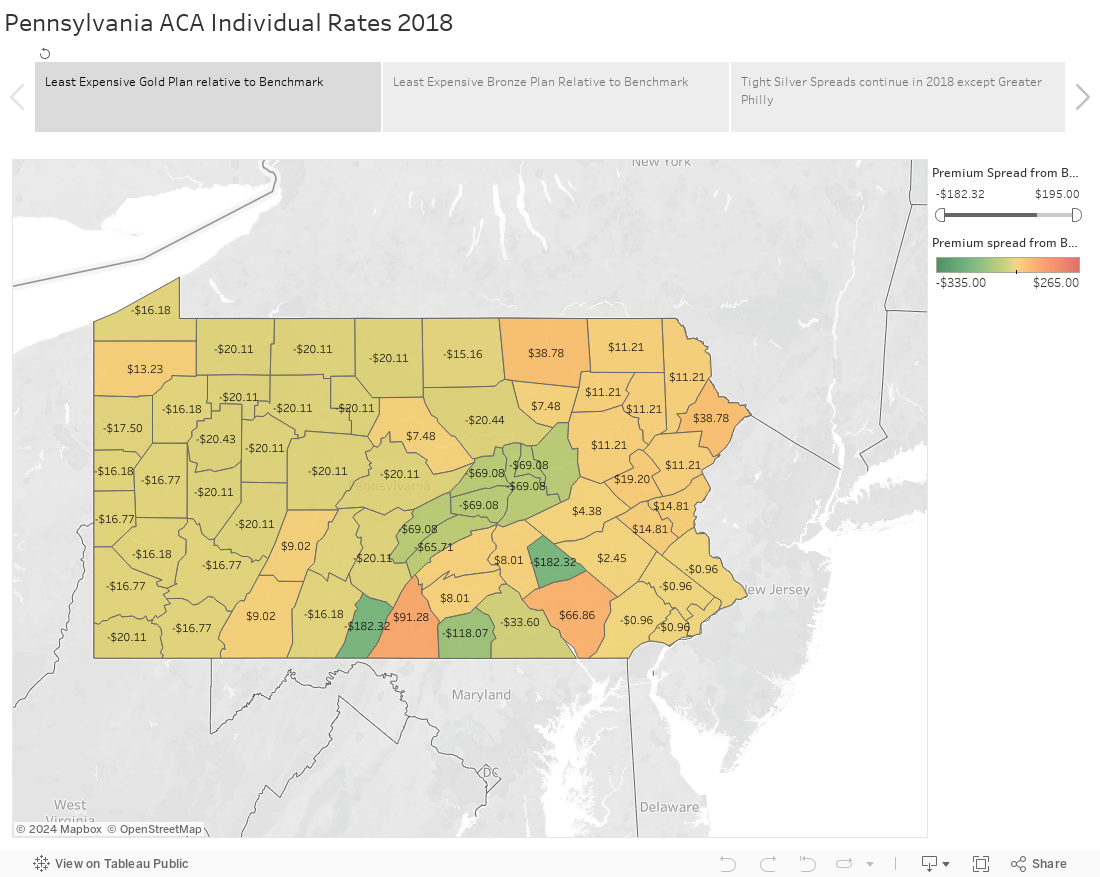

This is a really good short explainer of how people should shop in 2018. If you make more than 400% FPL, don’t even look at the exchanges. Use a broker or go direct to the websites of the insurers in your county and buy directly from them. If you make between 200% and 400% FPL, take a very hard look at Gold plans. In most counties, there will be at least one Gold plan that is less expensive than the Benchmark Silver plan.

Below is a Tableau that has most of the details of the entire Pennsylvania insurance market. My data is here as a .txt file. I started with the state data, stripped out the small group plan-county combinations. After that, I identified the APTC eligible plans. From there, I flagged the county level benchmark. I then calculated the distance from each plan-county combination from the benchmark plan for that county. A negative number means that Plan X is cheaper than the benchmark. All premiums are based on a 21 year old non-smoker who does not receive a subsidy. As people get older and families get larger, the spreads between Plan X and the benchmark will increase by a fixed ratio.

I have a few observations below the fold.