Here’s a photo of Patsy Marie from 2009:

As a mother I am ashamed to admit this, but it’s very possible I have more puppy photos of my dogs than I do baby photos of my kid.

Open thread!

Come for the politics, stay for the snark.

Here’s a photo of Patsy Marie from 2009:

As a mother I am ashamed to admit this, but it’s very possible I have more puppy photos of my dogs than I do baby photos of my kid.

Open thread!

With Monday’s revelations, we know more about Donald Trump’s Russian connections, but there is obviously more to come. As I urged in August, we need to think about options for the country’s response as this plays out.

David Roberts (@drvox) posted a tweetstream Sunday night on whether the country can come together, given the division sown by the Republicans and their implications of “Second Amendment solutions” and, potentially, civil war. Daniel Nexon (@dhnexon), a professor of political science, posted a similar, but shorter tweetstream. Roberts has now written a post that is still longer and goes in a different direction than I take here. I’ll work from the tweetstreams.

We who choose to surround ourselves

with lives even more temporary than our

own, live within a fragile circle;

easily and often breached.

Unable to accept its awful gaps,

we would still live no other way.

We cherish memory as the only

certain immortality, never fully

understanding the necessary plan.

— Irving Townsend

And while I’m grateful for all the thoughts, and I am still so broken about this sudden, unexpected loss, I know each and everyone of us has something going on that makes some days harder than others. And this place is where we can come for support, comfort and even some testy exchanges that keep us going. I will be always be in wonder and awe of everyone here and thankful John created such a place as Balloon-Juice.

Again, thank you for taking the time to leave me a note, it means more than you could ever know. I’ll give Bixby an extra hug from all of you, he’s having a difficult time, but he’ll bounce back. – TaMara

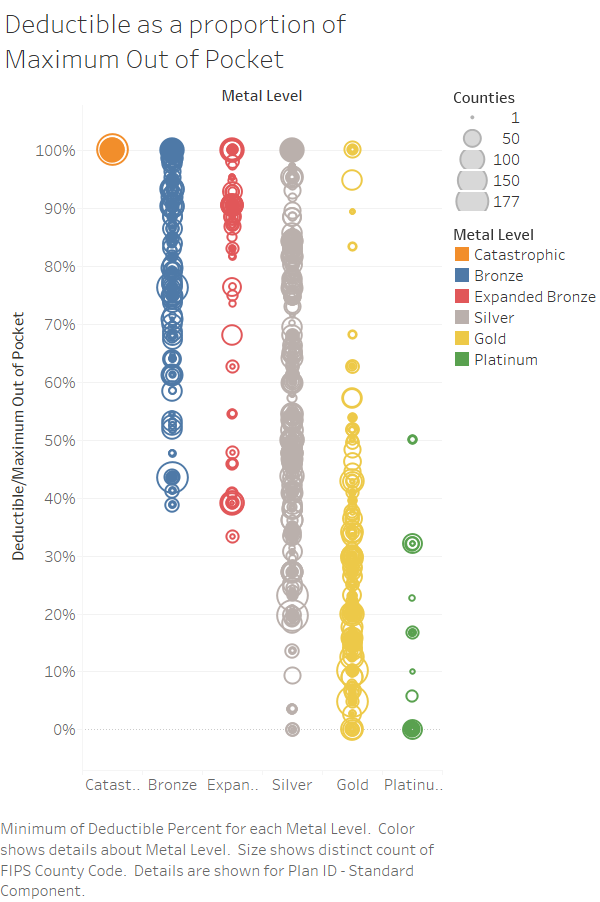

Within the ACA, plans are grouped into metal bands. Those bands have a target actuarial value with a band of allowed variance around that target. After a plan shows that it meets the allowed actuarial value without going the maximum out of pocket limit nor violating the non-cost sharing preventative services restriction, insurers are allowed to design their plans however they want.

There is wide variation in plan design. There are three cost sharing components. Deductibles are what the patient pays before the insurer will do more. Deductibles may apply to all services or only some services. Co-pays are fixed amounts that the patient pays for a given service. Co-insurance is a percentage that the patient pays. Once the total out of pocket spend meets the plan’s maximum out of pocket, the insurance company is on the hook for all claims above that limit.

Insurers can choose their plan designs and those choices have significant distributional impacts:

Deductible plans favor the sickest people as the low utilizers pay for almost all of their care via deductible cash. That means the proportion of the pool’s individual responsibility amount is borne by healthy people.

Co-pay only plans favor people who use highly concentrated cost services. A co-pay does not differentiate between a specialist visit with a contract expense of $200 and a specialist visit with a contract expense of $600. It is the same fee. So people who use very costly services but only rarely are best off. People who use a lot of fairly low costs services on a regular basis pay more proportionally.

Co-insurance only plans favor low cost utilizers. They are not paying full price via their deductible, and unlike co-pays, the individual cost per unit matters.

I was talking with a colleague about insurance in North Carolina earlier this week. There are 33 plans being sold on the Exchange. Twenty-seven of the plans have a maximum out of pocket expense (Max OOP) of $7,350. I expected to see that type of Max OOP for Catastrophic and Bronze plans. I would not have been surprised to see that Max OOP for Silver plans but I was surprised to see a $7,350 Max OOP for a Gold Plan. The lowest Max OOP was $6,650 for a Bronze plan where the entire cost sharing was the deductible.

We looked into the plans and saw that the deductible got lower as the AV increased as well as co-pays and co-insurance. The max-OOP translated to different levels of spending. The Bronze Plan Max-OOP was $6,650 before the insurer paid everything the Gold plan only paid some of the claims to just over $40,000 before the insurer had to pay everything. It is mainly a risk distribution bet on actuarial value as people who have a $10,000 claim are much better off in Gold than Bronze.

But as part of that discussion, I got curious about how much weight the deductible bears in cost sharing across the country. I used the Landscape PUF to calculate a rough metric: Individual Medical Deductible/Individual Medical Maximum Out of Pocket. If the quotient is 1, the deductible does all of the cost sharing. If the quotient is 0 there is no deductible. The Gold plan I mentioned above has a quotient of .17.

I’m seeing a few things. There is wild variance in plan design. Silver is all over the place. Zero dollar deductible plans are possible with Silver, Gold and Platinum. Low deductible plans are fairly common for those metal plans. They make up their cost sharing by co-pays and co-insurance. I need to go back over time and calculate this quotient in previous years before I can make strong statements. Right now it looks like plans of Silver/Gold/Platinum are being designed more often than not to look or actually be more attractive to healthier individuals.

Major trump donor Robert Mercer owes the IRS $7 billion in back taxes. https://t.co/dANmMeMZeW

— Anthony De Rosa ? (@Anthony) November 2, 2017

Does this have anything to do with Mercer stepping down from Renaissance? https://t.co/DUgX89t1Ct

— Emily Flitter (@FlitterOnFraud) November 2, 2017

We were all, understandably, agog yesterday over Robert Mercer’s sudden decision to step down from his hedge fund (and also cut Breitbart loose). But I was working my ADD-addled way through the tweetstreams late at night, and read for the first time about Mr. Mercer’s disagreements with the IRS:

… Suddenly, the government’s seven-year pursuit of Renaissance Technologies LLC is blanketed in political intrigue, now that the hedge fund’s reclusive, anti-establishment co-chief executive, Robert Mercer, has morphed into a political force who might be owed a big presidential favor.

With Trump in the Oval Office, Mercer and his daughter Rebekah, who has become his public voice, seem armed with political firepower every which way you look – and that’s even though presidential adviser Stephen Bannon, their former senior executive and political strategist, appears to have recently lost influence.

Since the IRS found in 2010 that a complicated banking method used by Renaissance and about 10 other hedge funds was a tax-avoidance scheme, Mercer has gotten increasingly active in politics. According to data from the Center for Responsive Politics, he doled out more than $22 million to outside conservative groups seeking to influence last year’s elections, while advocating the abolition of the IRS and much of the federal government.

The Mercer Family Foundation, run by Rebekah Mercer, also has donated millions of dollars to conservative nonprofit groups that have called for the firing of IRS Commissioner John Koskinen, an Obama administration holdover whose five-year term expires in November…

IRS leader Koskinen has said publicly that he intends to finish his term. On his watch, the agency hasn’t been cowed by the Mercers.

The IRS recently released a little-noticed advisory stating that its top targets in future business audits will include so-called “basket options,” the instruments that Renaissance and some other hedge funds have used to convert short-term capital gains to long-term profits that have lower tax rates…

More detail from an Oct. 27 Bloomberg article:

… Members of the Internal Revenue Service’s Office of Appeals are scheduled to meet with lawyers for Renaissance in New York on Nov. 7, according to a person with knowledge of the matter. The meeting kicks off a review by an independent branch of the tax agency and suggests a resolution may be years away.

Although the dollar amount at issue has never been made public, Senate investigators estimated that Renaissance employees may have pocketed about $6.8 billion through what a bipartisan panel in 2014 called an “abusive” tax shelter. Renaissance executives maintain the transactions at issue were within the law and weren’t driven by tax savings…

Trump named David Kautter to become acting IRS commissioner after the term of John Koskinen, an appointee of Barack Obama, expires Nov. 12. Kautter doesn’t require Senate confirmation. Rootstrikers, a group critical of the Trump administration, began a petition drive Friday opposing the Kautter appointment, calling it an “end run around the Senate” that “could lead to a massive payback for billionaire Trump donor Robert Mercer.”…

Things I Did Not Know: Mercer-nary Objectives?Post + Comments (119)

A new paper just was released in the Journal of Economic Perspectives that looks at the value of too much choice in health insurance (Erickson, Sydnor).** There are real costs to too much confusion as people will often make choices that are inefficient.

Insurers like inefficient choices. They want people who are likely to be very healthy and very low utilizers to buy low deductible, high premium insurance. If a highly probably low utilizer chooses a more expensive plan, that is more money that they are paying in premiums that is available to either cross subsidize high utilizers or hookers and blow.

On Healthcare.gov in 2018, the range of offered plans in each county goes from 2 plans in 6 counties to 119 plans in Seminole County Florida. Two plans are too few. 119 plans are too many. In 2017, the range was similar. Some of the variation is due to the number of insurers in a county. The more carriers in the county, the more plans we should expect. Even in single insurers counties, the number of unique plans ranges from 2 plans to 49 plans.

Some people have an easy choice. If they know that no matter what that they will have very high medical costs, their search criteria is first a function of network and then hassle factor before coming down to total costs. If the network is sufficient and hassle is similar people with high medical costs decide on the sum of net premiums and maximum out of pocket expenses. However most people don’t have those types of high cost conditions. They might have a blood pressure medication and see their cardiologist once a quarter as baseline costs but the major decisions are based on probabilistic thinking and how they interact with the varied cost sharing.

Most insurers are not stupid. The cost of designing plans once a baseline network is built and plan type established is fairly low. Creating twenty or thirty or forty different choices where the pragmatic meaningful difference is minimal means people will get confused. Confused people will either not buy or they will not buy optimal plans. And if they are not buying optimal plans that either means they are paying more in premiums than they should or they are paying more in out of pocket expenses than they should. Confused reasonably healthy buyers means the table is tilted towards the insurers. They are the experts who have people thinking about choice architecture and cognitive biases every day of the year.

** Ericson, K. M., & Sydnor, J. (2017). The Questionable Value of Having a Choice of Levels of Health Insurance Coverage. Journal of Economic Perspectives, 31(4), 51-72. doi:10.1257/jep.31.4.51

Folks, this will be the last feature for a while.

I’m destroyed.