Note: this post is a joint effort with colleagues who have closely tracked the CSR chaos induced by Trump and Republicans in Congress. Dave Anderson is a former health insurance analyst, now a healthcare scholar at Duke, and a blogger at Balloon Juice; Charles Gaba is the fabled chronicler and analyst of ACA enrollment, marketplace pricing, and healthcare policy; Louise Norris is co-owner of a unique mom & pop health insurance brokerage for individual market customers and a top source of marketplace information and analysis at her own blog (link in byline) as well as at healthinsurance.org and elsewhere. Andrew Sprung writes about healthcare policy on his blog, xpostfactoid, as well as at healthinsurance.org and other publications.

——————————————————————————————————————————————————————-

The open enrollment period for the 2018 ACA Marketplace that begins on November 1, 2017 is likely to confront enrollees with more challenges than any open enrollment since the troubled launch of the ACA Marketplace in October 2013. The time period is shorter, the outreach will be far less robust, and the pricing of plans will behave in ways that people do not expect. Much of the pricing variance will be a result of choices that states and insurers have made in response to the uncertainty over whether the federal government will continue to reimburse insurers for the Cost Sharing Reduction (CSR) subsidies that insurers are legally obligated to provide to qualified exchange enrollees.

In the ACA Marketplace, enrollees choose among plans grouped in four “metal levels” defined by actuarial value (AV), a measure of the percentage of average medical costs the plan will cover. Bronze plans provide coverage at 60 percent AV, Silver plans at 70 percent AV, Gold at 80 percent AV and Platinum at 90 percent AV.

CSR is available only to low income enrollees, and only with Silver plans. For low income enrollees, CSR boosts AV from a baseline of 70 percent to:

- 94 percent for enrollees with incomes up to 150 percent of the Federal Poverty Level (FPL)

- 87 percent for enrollees with incomes between 150 and 200 percent FPL

- 73 percent for enrollees with incomes between 200 and 250 percent FPL

At present, 57 percent of on-Marketplace enrollees access CSR, including over 80 percent of Silver plan enrollees. Silver plans are priced, however, as if the AV is 70 percent for all enrollees. Under threat that the Trump administration will stop reimbursing CSR, or that the courts eventually will order the administration to stop payment if Congress fails to appropriate the funds, states and insurers must decide how to enable insurers to cover the cost of providing the richer CSR-boosted coverage.

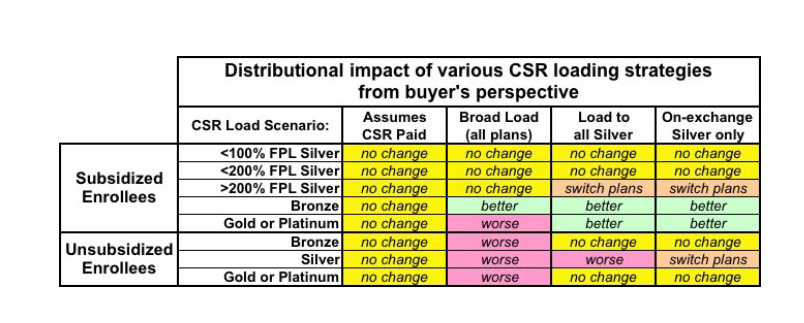

States and insurers have taken several approaches to managing to the CSR uncertainty. Some states have offered guidance or positive instruction, while others have left decisions entirely to insurers. The choices states and insurers have made will reshape the relative value of plans offered at different metal levels to various income groups — and determine who bears the brunt of the federal government’s potential abdication of responsibility for CSR reimbursement.

Among the choices made by states and insurers:

- Assume CSR is paid in a timely manner

- Assume CSR is not paid and load all costs onto plans at all metal levels.

- Assume CSR is not paid and load all costs only to all Silver Plans

- Assume CSR is not paid and load all costs only onto on-exchange Silver plans

- Insurers are required to sell any plan offered on the exchange off-exchange as well, but they may sell additional plans off-exchange. These off-exchange-only Silver plans would not have CSR costs loaded.

States are not required to impose one assumption on insurers. In New Mexico, for instance, some insurers have assumed that CSR will not be paid and have spread the costs through all metal plans. However, one New Mexico insurer, Molina, also assumed that CSR will not be paid but loaded all of the CSR costs into their Silver plan. This leads to a situation where the Molina Gold plan is less expensive than all Silvers and is comparably priced to all non-Molina Bronze plans. Georgia is also shaping up to be complicated, with one insurer assuming CSR funding will continue, and the rest assuming it won’t, but with varying approaches to loading the cost of CSR onto premiums.

The distributional consequences of these different choices are significant and varied.

State Approaches to Handling CSR Uncertainty for 2018 PremiumsPost + Comments (16)