I need to think this through on a screen. Let’s get a simple model on the buy/no buy decision. Let us make some absurd assumptions on a guaranteed issued, community rated plan. This is an absurd toy model to clarify my thinking.

1) Single insurance product only

2) No out of pocket expenses (Insurer pays 100% of every claim)

3) Contract is for a single period with future periods having their own buy/no buy decision points.

4) Risk aversion and risk tolerance can vary by individuals.

5) All premiums go straight to claims (no admin costs)

6) Premiums are All Claims/Number of people signed up

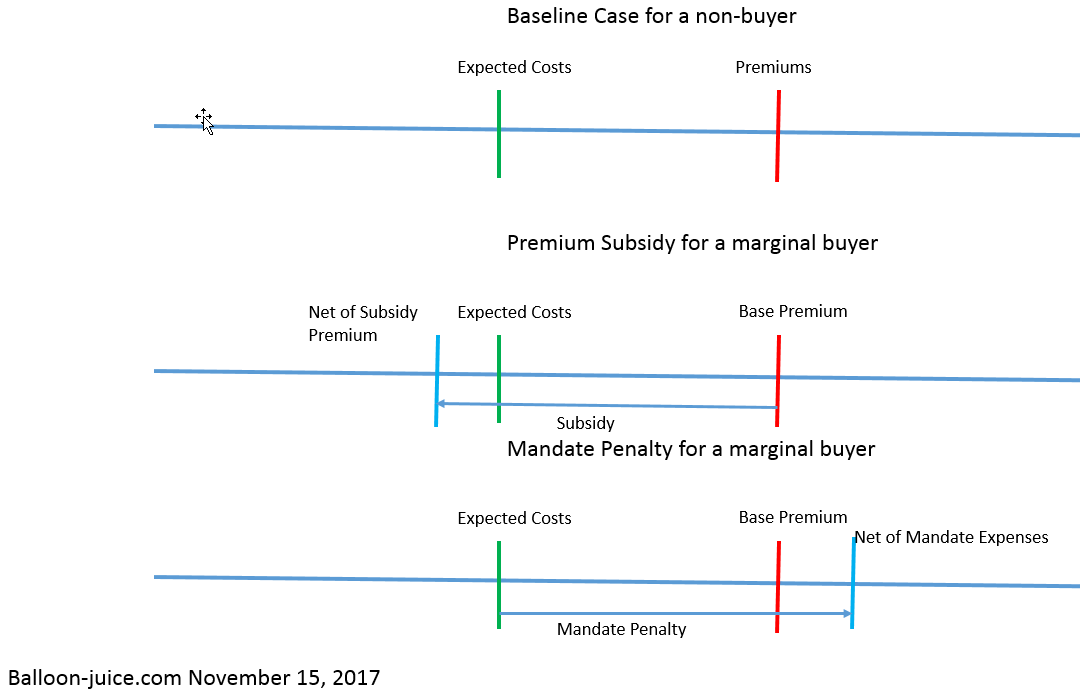

The decision is to buy a plan if the cost of premiums is less than or equal to expected medical costs. If premiums are less expensive than expected medical costs, insurance is bought. If premiums are more expensive than expected medical costs, insurance is not bought.

As you can see this sets up a death spiral as healthy people get out of the market and only sick people stay in. In the next round, the healthiest of the sick people leave the market and only the sickest of the sick stay in. Oops.

There are two levers that can counter-act or stop this spiraling. They both change the relative price of not being covered instead of being covered. Subsidies lowers the relative price spread by reducing the cost of being insured. An individual mandate penalty increases the cost of being uninsured. Both of these are attempts to move more low cost people from the no buy pool to the buy pool.

This is an absurd oversimplification but I think it is a useful oversimplification.

Once we think about assumption #6, we see that premiums are a function of other people’s decisions to buy or not buy. As more healthy people buy plans, they add incrementally less than average claims costs and bring down average premiums for everyone. One individual with absolutely no claim expenses in a year will not move the needle much, but hundreds or thousands of people with a few hundred dollars a year in claims will make premiums lower for everyone else.

Talking through Subsidies and Mandates on buy-no buy decisionsPost + Comments (5)