ACA open enrollment is starting at the end of the week. The 2020 Open Enrollment Period will be one with more choices than the past couple of years with significant premuium swings. There are no major changes in outreach activities budgeted for by Healthcare.gov. The advertising and navigation budget is very low but not too different from their 2019 Open Enrollment Period budget. Beyond insurer entry and exit and plans being terminated and created, the big source of variation will be in the post-subsidy premiums. Subsidized buyers, and more importantly, the marginal subsidized buyer who is flipping a coin as to whether or not they will be covered next year, are primarily concerned about the premium that they pay every month and little else. This means that they care about the spread between the cheapest plan available to them and the benchmark plan. This is the “Silver Gap” game I’ve been talking about for years now.

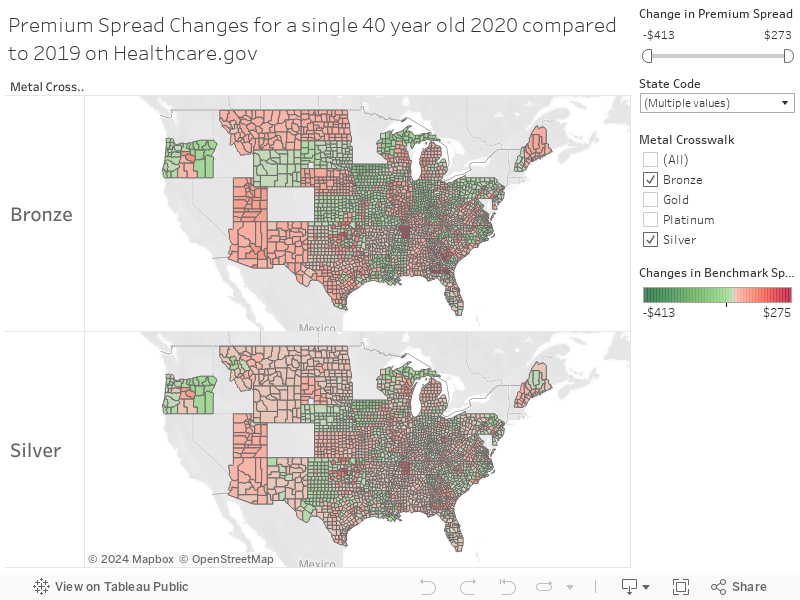

There is significant variation. The maps below show the difference in premium spreads between the cheapest Bronze and Silver plans to the county benchmark for 2019 and 2020. Green shows that a county has a cheaper net of subsidy plan now available in 2020. Red shows that the premium spread has shrunk and therefore the cheapest subsidized plan in that metal level for that county is now more expensive net of subsidy. Bronze plans will be the cheapest plans, while silver plans will have high Cost Sharing Reduction (CSR) enhancements added which makes these the overwhelmingly dominant choice for people earning between 100-200 percent of the Federal Poverty Level (FPL).

All else being equal, we should expect to see enrollment overperformance in northern Iowa, Oregon, the Upper Pennisula of Michigan. We should expect to see enrollment underperformance in parts of Oklahoma, most of Utah, Appalachian Kentucky, Western Tennessee, Southern Ohio, the coast of Wisconsin among other areas. These are rough directional estimates. There are twelve counties in Oklahoma that have seen their bronze to benchmark gap be reduced by over $150 for a single forty year old. That would, naively, lead to expectations that enrollment for healthy individuals earning over 200% FPL would crash. However the 2020 bronze to benchmark spread is still large enough to make a zero premium plan available.

However, as a first rule of thumb, big changes in premium spreads between the cheapest plans and the cheapest silver plans relative to benchmark will give us a good intuition as to which counties will see significant changes in enrollment for 2020.

Where to expect enrollment swings on Healthcare.govPost + Comments (8)