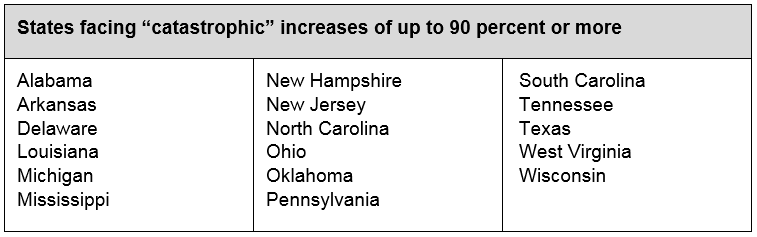

Covered California released an actuarial study on the premium changes for the ACA individual insurance market due to policy changes over the past six months. It is ugly. The premiums will vary greatly by state over the next three years according to this study. I just want to look at the worst states.

Senator Cassidy (R-LA) repeatedly brought up the story of one of his constituents last year. They were a family of four with total earnings in the the six figures. They did not qualify for premium tax credits even as they were spending $40,000 a year in total medical costs. One family member has a chronic, high cost medical condition. This person could never pass underwriting.

This family will face a choice of paying over half their income for premiums by 2021 under the current policy regime or aggressively finding ways to lose enough income to get under 400% FPL to qualify for a premium tax credit that caps their Silver premium expense at less than 10% of their income. Given the much higher premiums, the opportunity cost of financial engineering to qualify for a premium tax credit will go down. Having a family member with an expensive chronic condition under the current policy regime places a huge notch on earnings between 400% and 600% FPL where almost every additional dollar earned would go to either taxes or individual market premiums.

The critical question in any health financing system is how are the people with consistent and known high cost needs treated. Are they left on their own? Are they shunted aside? Are they consigned to a life of poverty? Or is there a system that counter-acts the bad luck that they have so the opportunity space is as broad and deep for them as it is for anyone else.

Right now the health policy proposals floating around Washington for the past year narrows opportunity space for many people