As part of a very interesting discussion on the underlying ethics of the American health insurance direction, there was an interesting set of tweets that I want to explore some more here:

@MDaware @ddiamond @uereinhardt and the same payer

— Richard Mayhew (@bjdickmayhew) July 23, 2016

From a provider point of view, the fragmented payer market is an excellent opportunity for providers to segment the market. I was speaking with a friend of mine whose a neurologist and she said that her office manager routinely juggles a dozen different insurers. She did not pay attention to what the individual insurers paid per product, she just saw the patients who her scheduler put on her schedule.

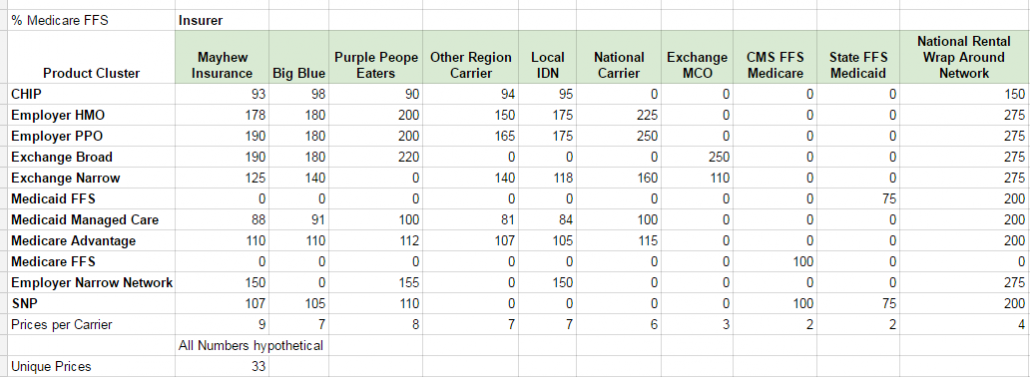

Below is a hypothetical pricing chart by insurer and product line that a typical doctor could see in the course of day. The numbers are hypothetical but close enough.

Yes, this is confusing as hell for the patient as they have no idea what they are getting. It is confusing as hell for the doctor’s back office. It is confusing as hell for the insurance company.

It is also an attempt to segment the market. We talked about provider account receivable preferences before where docs want to fill their schedule first with high paying, no questions asked commercially covered people, then Medicare as they pay fast, then Exchange plans, then CHIP and then finally Medicaid. That was a general statement. Providers or their schedulers will often give the marginal appointment slot to one or two particular commercial payers instead of any and all commercial payers.

The more segmented the market the theoretically ‘efficient’ it is but all of these pricing decisions are amazingly non-transparent so I have no idea how to math out an efficiency argument here.